From Dallas and Minneapolis to New York and Los Angeles, offices sit vacant or underused, showing the staying power of the work-from-home era. But clear desks and quiet break rooms aren’t just a headache for bosses eager to gather teams in person.

Investors and regulators, on high alert for signs of trouble in the financial system following recent bank failures, are now homing in on the downturn in the $20 trillion US commercial real estate market.

Just as lenders to the sector grapple with turmoil triggered by rapidly rising interest rates, the value of buildings such as offices is crashing. That could add to pain for banks and raises concerns about damaging ripple effects.

“Although this is not yet a systemic problem for the banking sector, there are legitimate concerns about contagion,” said Eswar Prasad, an economics professor at Cornell University.

In the worst-case scenario, anxiety about bank lending to commercial real estate could spiral, prompting customers to yank their deposits. A bank run is what toppled Silicon Valley Bank last month, roiling financial markets and raising fears of a recession in the United States.

Asked about the danger posed by commercial real estate, Federal Reserve Chair Jerome Powell said last month that banks remained “strong” and “resilient.” But attention is growing on the links between US lenders and the property sector.

“We’re watching it pretty closely,” said Michael Reynolds, vice president of investment strategy at Glenmede, a wealth manager. While he doesn’t expect office loans to become a problem for all banks, “one or two” institutions could find themselves “caught offside.”

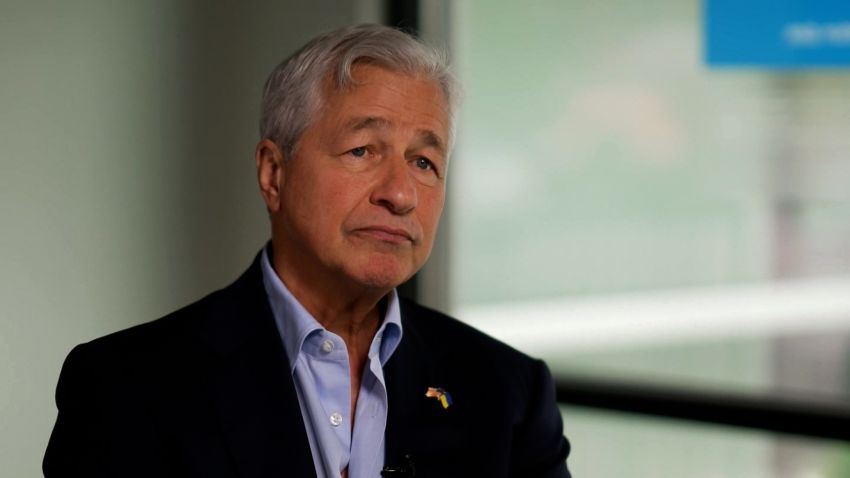

America’s top banker, JPMorgan Chase (JPM) CEO Jamie Dimon, told CNN Thursday that he couldn’t be sure whether more banks will fail this year. Yet he was quick to point out that the current situation was very different to the 2008 global financial crisis, when there were “hundreds of institutions around the world with far too much leverage.”

The US market looks most vulnerable. Yet the European Central Bank and Bank of England have also recently warned of risks tied to commercial real estate as the outlook for prices deteriorates.

Work-from-home bill comes due

Commercial real estate — which spans offices, apartment complexes, warehouses and malls — has come under substantial pressure in recent months. Prices in the United States were down 15% in March from their recent peak, according to data provider Green Street. The rapid increase in interest rates over the past year has been painful, since purchases of commercial buildings are typically financed with large loans.

Office properties have been getting hammered the hardest. Hybrid work remains popular, affecting the rents many building owners can charge. Average occupancy of offices in the United States is still less than half March 2020 levels, according to data from security provider Kastle.

“You have fundamentals under pressure from work from home at a time when lending is less available than [it has been] over the last decade,” said Rich Hill, head of real estate strategy at Cohen & Steers. “Those two factors will lead to a pretty significant decline in valuations.”

Trouble may build as the economy slows. Hill thinks US commercial property valuations could fall roughly 20% to 25% this year. For offices, declines could be even steeper, topping 30%.

“I’m more concerned than I’ve been in a long time,” said Matt Anderson, managing director at Trepp, which provides data on commercial real estate.

Signs of strain are increasing. The proportion of commercial office mortgages where borrowers are behind with payments is rising, according to Trepp, and high-profile defaults are making headlines. Earlier this year, a landlord owned by asset manager PIMCO defaulted on nearly $2 billion in debt for seven office buildings in San Francisco, New York City, Boston and Jersey City.

What it means for banks

This is a potential problem for banks given their extensive lending to the sector. Goldman Sachs estimates that 55% of US office loans sit on bank balance sheets. Regional and community banks — already under pressure after the failures of Silicon Valley Bank and Signature Bank in March — account for 23% of the total.

Signature Bank (SBNY) had the tenth biggest portfolio of commercial real estate loans in the United States at the start of the year, according to Trepp. First Republic (FRC), which received a $30 billion lifeline last month from JPMorgan Chase and other major banks, had the ninth largest. But both had a much a greater share of their assets tied up in real estate than bigger rivals such as Wells Fargo (WFC), the leading US lender to the sector.

The rise in commercial property prices over the past decade has provided developers and their bankers with a measure of protection. But pain could increase in the coming months.

About $270 billion in commercial real estate loans held by banks will come due in 2023, according to Trepp. Roughly $80 billion, nearly a third, are on office properties.

Plummeting valuations will make refinancing tougher for property owners, who are likely to face requests from banks to put up more equity. Some owners — especially of older, less desirable office buildings — might decide it’s not worth the expense given the market climate and simply hand back the keys.

Banks may prefer that option to kickstarting drawn-out, expensive foreclosure processes. But it puts them in the difficult position of owning depreciating properties.

“That is a scenario we will see now very often,” Christian Ulbrich, chief executive of global commercial real estate services giant Jones Lang LaSalle (JLL), told CNN. The question, he continued, is what lenders will do in that situation, and whether banks are sitting on such sizable loan portfolios that they need to take “significant losses.”

Keeping watch

Banks have less capacity to stomach financial blows these days. Smaller institutions are grappling with outflows of deposits to larger peers and money-market funds offering better returns. Plus, bank investments in government bonds, once considered low-risk, are notching up losses as interest rates climb.

The worst outcome, according to Neil Shearing, chief economist at Capital Economics, is that a “doom loop” develops. Questions about the health of banks with sizable exposures to commercial real estate loans cause customers to pull deposits. That forces lenders to demand repayment — exacerbating the sector’s downturn and further damaging the banks’ financial position. That triggers more deposit outflows in a “vicious cycle.”

That is not the central expectation right now. Since the 2008 financial crisis, banks have tightened lending standards and diversified their clientele. Loans for offices account for less than 5% of US banks’ total, according to UBS. And Ulbrich of JLL said that while the speed at which borrowing costs have risen has put significant pressure on the commercial real estate industry, it has lived with rates at this level for “most of its history.”

“There’s always a risk for self-fulfilling prophecies here, but I would still be fairly optimistic things will play out in a digestible way,” Ulbrich said.

The likeliest outcome is thought to be an uptick in defaults and reduced access to funding for the commercial real estate industry. Banks, it’s predicted, will weather the storm, though their earnings may take a beating.

That doesn’t mean, however, there won’t be spillovers.

“Distress of this type has historically not only hurt the landlords and the bankers who lend to them,” Lisa Shalett, chief investment officer at Morgan Stanley Wealth Management, said in a note to clients this month. Non-bank lenders, related businesses and investors may also be hurt, she said.